Chapter 10: The Last Lifeline — When the Giants Personally Tear Down Their Own Stress Test Arenas

On February 23, 2026, Phil Spencer retired.

Thirty-eight years at Microsoft. The last spokesperson for the Xbox brand trusted by players handed over the keys to his office. The person replacing him was Asha Sharma—the former vice president of Microsoft's CoreAI product division. An AI executive taking over a gaming division.

On the exact same day, Xbox President Sarah Bond also left Microsoft.

Two years prior—in January 2024—Microsoft had just finished spending $69 billion to complete the largest gaming acquisition in human business history, buying Activision Blizzard. Three months later, it laid off 1,900 people. In May, it closed Tango Gameworks—the developer of Hi-Fi Rush, a Game of the Year nominated title whose studio was disbanded before they even had time for a victory party. On the same day, it closed Arkane Austin—creators of the Prey and Dishonored series. In September, another 650 people were laid off. In July 2025, another wave: The Initiative closed, the Perfect Dark reboot canceled, Everwild canceled, and Turn 10 laid off nearly half its staff.

Seamus Blackley—co-creator of the first Xbox in 2001, the man who appeared in Chapter 3—used a phrase on social media: palliative care.

End-of-life care.

A console, from its birth in Chapter 3 to palliative care, walked a twenty-five-year journey. An arc from an OS defense weapon to an AI sacrifice drew to a close on the day Spencer retired.

But Xbox isn't the only machine being dismantled.

On the other side of the Pacific, Sony was doing the exact same thing—just using a different excuse.

I. Two Ways to Demolish

Microsoft's way of dismantling Xbox is to tear it down in broad daylight.

Chapter 3 explained the DNA of the Xbox: it is a wall, not a city. The function of a wall is to block invaders—Sony's PS2 threatened the living room flank of Windows, so Gates built a console to block it. Twenty-five years later, Satya Nadella judged that the living room was no longer a battlefield worth defending. AI was.

So the wall was torn down, and the bricks were moved to build another wall.

The $69 billion Activision games were released on PlayStation. Xbox exclusive games were opened up one by one. The hardware team was laid off. Studios were closed one by one. Every step had clear business logic: the gaming division's resources are being systematically transferred to AI infrastructure.

In fiscal year 2025, Microsoft's capital expenditures exceeded $100 billion—almost entirely directed toward AI data centers. It invested $13 billion in OpenAI. OpenAI promised to purchase $250 billion in Azure cloud services from Microsoft. The magnitude of these numbers makes all of Xbox's losses over twenty-five years look like pocket money.

Nadella's logic is simple: the revenue Xbox generates annually is not in the same order of magnitude as the revenue AI could potentially generate. Between a shrinking gaming hardware market and an AI platform that could reshape human productivity, where should the resources go?

From a CEO's perspective, this decision is unassailable. From the perspective of this book, this decision is tearing down an invisible brick.

But Sony's demolition method warrants a closer look. Because Sony wasn't tearing down a wall—it was tearing down a city.

II. Fourteen Days

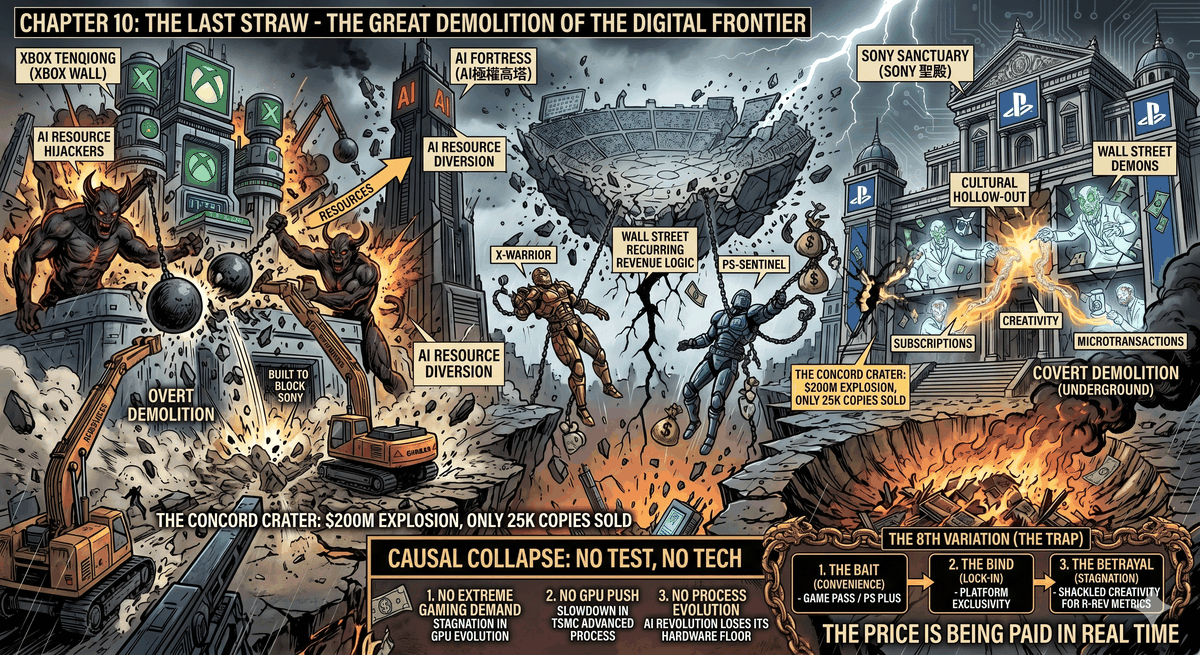

On August 23, 2024, Sony released a game called Concord.

A hero shooter. Full price at $40. Developer: Firewalk Studios—a studio Sony had just spent money to acquire in April 2023. Development cycle: over eight years. Reported R&D costs ranged from $200 million to $400 million; the industry generally estimated it at well over $200 million.

After launch, the peak concurrent player count on Steam was under 700. Combined sales across PS5 and PC were estimated at roughly 25,000 copies.

Fourteen days later—on September 6, 2024—Sony pulled Concord from all digital storefronts and offered full refunds.

On October 29, 2024, Sony announced the permanent closure of Firewalk Studios. All 174 employees were laid off. The game would not be brought back online, nor would it be reworked and relaunched.

Over $200 million in R&D investment. 25,000 copies sold. A fourteen-day lifespan.

This wasn't a commercial failure. This was an autopsy report.

And Concord wasn't an accident. It was the inevitable product of a systemic decision.

III. The Mirage of Live-Service Games

To understand why Concord existed, one must first understand Jim Ryan.

Ryan took over as CEO of Sony Interactive Entertainment in 2019. In 2022, he announced a radical strategic pivot: Sony would launch more than ten "live-service games" by fiscal year 2025.

The commercial logic of live-service games is as seductive as a drug to Wall Street.

The revenue model of traditional single-player games is a one-time transaction: the player pays $70, the developer collects the money, end of story. To make another lump sum, you have to develop a sequel from scratch—another three-to-five-year development cycle, another multi-hundred-million-dollar investment, another gamble.

The revenue model of live-service games is recurring income: the game launches for free or at a low price, and then continuously extracts money via season passes, virtual currency, and character cosmetics—so-called "microtransactions." A successful live-service game can be continuously harvested for five to ten years. A single year's revenue from Fortnite exceeds the lifetime revenue of many AAA blockbusters combined.

What Ryan saw were the numbers on the balance sheet. What he didn't see was the graveyard behind the balance sheet.

The cruelty of the live-service game market lies in this: It is winner-takes-all. A player only has so many hours in a day. He is already playing Fortnite, already playing Apex Legends, already playing Valorant—all for free. You want him to drop the game in his hands and spend $40 to buy a brand new hero shooter he is completely unfamiliar with? Why would he?

But Ryan didn't care about this problem in 2022. He cared about how Wall Street viewed Sony's revenue structure. One-time transactions vs. recurring income—in the language of the capital markets, the former is called "unpredictable," and the latter is called "high-quality revenue." Shift more revenue from one-time to recurring, and the price-to-earnings (P/E) ratio goes up, and the stock price goes up.

Here, that pattern appears again. Only this time, the convenience isn't for the players; it's for Wall Street.

Ryan issued the order in 2022. Sony's first-party studios began to be required to make live-service games. Not a suggestion; a directive.

Naughty Dog—creators of The Last of Us—were required to make a The Last of Us multiplayer online game. After years of development, it was ultimately canceled.

Insomniac—developer of Spider-Man—made an online game called Spider-Man: The Great Web. Canceled.

Bend Studio—developer of Days Gone—submitted a sequel pitch. Rejected. The team was reassigned to support the live-service development of other projects.

Bluepoint Games—a studio Sony acquired in 2021, famous for the Demon's Souls remake—was required to make an online God of War. The project was ultimately canceled, and in February 2026, Sony announced the closure of Bluepoint.

Japan Studio—Sony's founding studio in Tokyo, the cradle of the PlayStation brand—was closed in April 2021. Former PlayStation executive Shuhei Yoshida later revealed he was removed from his position because he refused to execute Ryan's directives.

One by one. Studio by studio.

The first-party studio ecosystem Sony spent thirty years building—one of the most powerful single-player game development networks in the world—was systematically dismantled in three years. Not because these studios couldn't make good games. It was because the genre of games they made was not the revenue structure Wall Street wanted to see.

Ryan retired in March 2024. The report card of his live-service strategy was already clear by then: the collapse of Concord, the cancellation of multiple projects, the closure or restructuring of several studios. The only bright spot was Helldivers 2—but that was a game already in development before the strategic pivot, not Ryan's credit.

Ryan had real power. Ryan had a direction. Ryan's direction had been proven wrong.

But we must pause here and ask an uncomfortable question.

Did Ryan really lose?

From the players' perspective, yes. From the PlayStation brand's perspective, yes. But from Wall Street's perspective—Jim Ryan was a textbook-successful CEO.

During his tenure, Ryan did several things the capital markets welcomed extremely warmly. First, he moved the core of power and headquarters of Sony Interactive Entertainment from Tokyo to San Mateo, California—a perfect American tech company corporatization. His compensation structure was highly dependent on performance-linked stock options; as long as the revenue on the financial reports hit new highs, he personally made a fortune. Second, he forcefully pushed the porting of PlayStation exclusives to PC—players saw this as a "betrayal" of the exclusivity promise, but Wall Street saw "one asset, earning money twice." Killing two birds with one stone, profits instantly doubled. Third, he exited with perfect timing in March 2024—perfectly dodging the light-speed collapse of Concord five months later, while using the layoff of 900 people and the closure of the London Studio to "dress up the books" right before he left.

Ryan left behind a bloated mess of live-service games. But he took with him wealth he couldn't spend in several lifetimes.

This is not moral criticism. It is a structural observation. In the governance logic of a publicly traded company, Ryan perfectly fulfilled his fiduciary duty to shareholders—maximizing shareholder value during his tenure. As for the soul of PlayStation, the demise of Japan Studio, the $200 million turning to ashes with Concord—these are not in the formula for calculating shareholder value.

And hidden here is a deeper contrast.

In 1999, the man standing on the stage at the PS2 launch event—Ken Kutaragi—and Jim Ryan were completely opposite species. Ken Kutaragi was an engineer. He personally designed the Emotion Engine chip, using floating-point performance data to force Gates into building the Xbox (the story of Chapter 3). He defined the gaming ecosystem with technological romance, using the limits of hardware to ask, "What else can gaming become?" He ultimately failed too—the PS3's Cell processor was too radically designed, its development difficulty scaring off the entire third-party market—but his failure was an engineer's failure: betting on technology, losing on technology.

Ryan didn't bet on technology. Ryan bet on financial statements. In his eyes, PlayStation wasn't a hardware platform; it was a revenue pipeline. He didn't care how much artistic soul Japan Studio's Gravity Rush or ICO had—he cared about the "monthly active users" and "profit margins" of those games. When the numbers weren't met, the studio was closed. When Wall Street said recurring revenue was good, all studios pivoted to live-service games.

Ken Kutaragi didn't destroy Sony's financials. Ryan didn't destroy Sony's financials either. What Ryan destroyed was the soul of PlayStation—he turned a hardware kingdom built by an engineer into a vulgar, American-style content distribution platform.

And the coldest fact is: in the language of the capital markets, "destroying the soul" is not a KPI. No analyst will ask you on an earnings call: "Does your platform still have a soul?"

IV. Three Mirrors

Now let's put the three CEOs together.

Pat Gelsinger. Lisa Su. Jim Ryan.

The conclusion of Chapter 9 was: The victors of tech history are not the smartest people, they are the ones in the right system, holding enough real power, who dare to bet everything.

That conclusion is correct. But incomplete.

Because it only answered "why some people win." It didn't answer "why some people lose"—and there is more than one way to lose.

Gelsinger's failure: No real power. Chapter 9 has already analyzed this in detail. Intel's MDF system and one-stop service teams had solidified into interest groups. Gelsinger saw all the problems, but he couldn't move the machine. Wall Street didn't give him time, and the board didn't give him the knife. His prescription was completely correct—IDM 2.0, rebuilding manufacturing, catching up to TSMC—but the patient refused to take the medicine.

Ryan's failure: Real power, wrong direction. Ryan's power at Sony was unchallenged—he could close Japan Studio, replace Shuhei Yoshida, and order Naughty Dog to make online games. No interest group could stop him. But he pushed the entire company in a direction that Sony's DNA did not support. Sony's moat was single-player narrative games—The Last of Us, God of War, Uncharted, Ghost of Tsushima. The capabilities required for live-service games—live operations, community management, continuous production of seasonal content—were muscles Sony had never built. Ryan made a group of marathon runners enter a boxing match.

Nadella's gamble: Real power, undetermined direction. Nadella is the most powerful of the three—he controls a company worth over three trillion dollars, and the board trusts him completely. His logic in shifting Xbox's resources to AI is, from a business perspective, unassailable. But the return cycle for AI investment is unknown. A $100 billion annual capital expenditure—what if the commercialization of AI is three years slower than expected? What if OpenAI's technology is surpassed by Google or Anthropic? What if the AI bubble bursts?

Gelsinger had the right prescription, but the system wouldn't let him take it. Ryan's system let him do anything, but the prescription he wrote was poison. Nadella's system lets him do anything, and his prescription might be right—but the bill won't be known for another five years.

Three modes of failure. Three mirrors. But they reflect the exact same image.

V. The Same Root Cause of the Disease

Microsoft dismantled Xbox. Sony dismantled studios. On the surface, the two companies were doing completely different things—one chasing AI, the other chasing live-service games.

But if you step back and look closely at the logic of their decisions, you will find that what drives these two decisions is the exact same spell cast by the capital markets.

Turn one-time transactions into recurring revenue.

Microsoft's version: Turn the sale of game consoles (a one-time hardware transaction) into selling Game Pass subscriptions (recurring monthly fees), and then into selling AI cloud services (recurring enterprise contracts). Every step makes the revenue structure look "higher quality" in the eyes of Wall Street. Nadella slashed nearly half the staff of Turn 10 Studios—the development team behind the ForzaTech engine, one of Xbox's last remaining low-level technical vanguards—and simultaneously used the saved money to buy NVIDIA GPUs to build AI data centers. Because AI's price-to-dream ratio is high, Wall Street loves to see it.

Sony's version: Turn the sale of a $70 single-player game (a one-time purchase) into the microtransactions of a live-service game (recurring consumption). Ryan butchered single-player studios and forced all teams to pivot to live-service games. Because the P/E ratio for recurring revenue is higher than for one-time buyouts, Wall Street loves to see it.

Two paths, one destination: paying protection money to Wall Street.

This is not a metaphor. CEOs of publicly traded companies have a fiduciary duty to shareholders—to maximize shareholder value. If Wall Street believes recurring revenue is worth a higher P/E ratio than one-time transactions, then all CEOs have an obligation to push their revenue structures in that direction. A CEO who doesn't push will be replaced—Chapter 9's Gelsinger is a living example.

Nadella wasn't "wrong." Ryan wasn't "wrong." They both perfectly fulfilled their responsibilities to shareholders as CEOs of publicly traded companies. But the cost was that they personally dismantled the invisible supply chain described in Chapters 7 and 8.

And this is exactly what is most terrifying: Under the logic of capital, destroying the cornerstones of technology is actually the "most rational and profitable" behavior.

This logic has a fatal blind spot.

It assumes that gaming is merely a commodity—a revenue stream that can be repackaged, repriced, and reallocated. It doesn't care what role gaming plays in the broader technological ecosystem.

This book has spent nine chapters explaining that role.

Chapter 7: Gamers' money fed CUDA. Inside every GeForce sold were general-purpose compute cores gamers didn't use, amortizing ten years of R&D costs for the AI revolution.

Chapter 8: Gaming GPUs are the stress test arena for TSMC's advanced processes. The 608-square-millimeter die of the RTX 4090—five and a half times larger than an iPhone chip—forced TSMC to push the yield of its 5nm process to the absolute limit. Without this stress test, the H100 could never have been mass-produced.

Chapter 8 also stated another fact: Console SoCs are TSMC's invisible ballast. Orders for the PS5 and Xbox Series X—lasting seven to ten years and shipping tens of millions of units—filled the capacity voids during the iPhone's off-season, keeping fab utilization at high levels. This was one of the prerequisites for TSMC daring to pour astronomical capital into building next-generation nodes.

Gaming is not a commodity. Gaming is a stress test arena plus an R&D funding pool. The cost of tearing it down won't appear on this year's financial reports. The cost will only materialize five or ten years from now.

And Microsoft and Sony are tearing it down simultaneously. Both CEOs are paying protection money to Wall Street. The names of the premiums are different—one is called AI, the other live-service games—but the bricks being torn down come from the exact same wall.

VI. Closing Arguments

That pattern appears for the last time. The eighth time. And the most dangerous time.

Because the previous seven variations locked in other people—consumers, developers, AI researchers, OEMs. And the ones tearing down the walls were also other people—Valve, AMD, the open-source community.

This time, the ones tearing down the wall are the owners themselves.

Microsoft is dismantling Xbox. Sony is dismantling studios. Both companies are using the same reason: We need to put our resources into more valuable places. Microsoft says that place is AI. Sony says that place is live-service games.

But the things they are tearing down—long-term chip orders for tens of millions of consoles annually, a consumer hardware market pushing the extreme limits of GPU performance, the demand for stress tests that forces TSMC to push yields to the extreme—these things are not on their balance sheets. What they are tearing down is an invisible supply chain stretching from the gamer's pocket to the silicon of AI chips.

The logic of Chapter 8 works like this: Gamers spend $1,599 to buy an RTX 4090 → NVIDIA uses this money to place large-die orders with TSMC → TSMC uses these orders to hone large-die yields → Once yields mature, they are used to build the H100 → The H100 drives global AI training.

The starting point of this chain is gaming. If the console market shrinks—if Xbox becomes a brand label instead of a piece of hardware—that chain loses a link. Long-term orders for console SoCs shrink, and TSMC's capacity balancer loosens. If the consumer GPU market is eroded by cloud streaming, NVIDIA's gaming revenue drops, and the base for amortizing the R&D tax shrinks—the cost of every AI card will rise.

No one has ever asked this question in the boardrooms of Microsoft or Sony. Because this chain is too long. Between the layoffs at Xbox and the capacity planning at TSMC, there are too many layers. And Wall Street only looks at the next quarter.

Convenience attracts Wall Street (higher P/E ratios) → Wall Street's pressure locks in the CEO's decision space → The CEO tears down gaming assets to feed AI or live-service games → Gaming's function as a stress test arena and R&D funding pool is weakened → The cost of this weakening only materializes five to ten years later → But by then, the things torn down can never be brought back.

In the previous seven variations, the cost of the pattern was reversible—at least theoretically. Microsoft could re-invest in DirectX. NVIDIA could open-source CUDA (though it won't). TSMC could take on new clients.

This time is irreversible. You can build a fab in three years, but you cannot rebuild the creative culture of a disbanded game studio in three years. You can spend money to hire back engineers, but you cannot buy back the unspoken chemistry between a team that has honed the same IP for a decade. Japan Studio is closed, and it stays closed. Tango Gameworks was picked up by Krafton. Arkane Austin is scattered. Bluepoint is scattered. The capabilities of these teams—to make games like Prey, Hi-Fi Rush, Demon's Souls, and Bloodborne that are revered by hardcore players as masterpieces, that drive hardware sales, and that force GPUs and CPUs to push their performance to the absolute limit—cannot be bought back with money.

Gaming is the stress test arena for technological evolution. And that stress test arena is being personally torn down by its owners. Not because of foreign invaders, but because the owners feel the land is worth more if used to build something else.

VII. The Loot is Still Being Divided

Back to February 23, 2026. Phil Spencer retires. Asha Sharma takes over.

A gaming journalist wrote a sentence in an article: "The soul of Xbox has left the building."

But the soul never lived in that building to begin with.

Chapter 3 already stated it: Xbox was never built for the players from day one. It was built to block Sony's threat to Windows. A wall, not a city. The people living behind the wall—the players who bought the Xbox, subscribed to Game Pass, and trusted the exclusivity promises—their investment was never on Microsoft's balance sheet.

Did Spencer know this? Probably. But he stayed for thirty-eight years, held on until the very last moment, and then handed the keys over to an AI executive.

Sony's situation is more complex. Because PlayStation truly was a city—a city with residents, culture, and a sense of belonging. The developers of Japan Studio, the writers of Naughty Dog, the craftsmen of Bluepoint—they weren't chips; they were residents. Jim Ryan used Wall Street's logic to tear down several walls of this city, and then retired. The people left behind are picking up the pieces.

But picking up the pieces does not equal rebuilding.

Because what was torn down weren't just studios. What was torn down was a signal—a signal telling game developers worldwide: in the eyes of major platform holders, your work is merely a revenue genre. If your revenue genre isn't the kind Wall Street prefers, you are a replaceable part.

The long-term effect of this signal runs deeper than any layoff. Because it changes the flow of talent. The best game developers will ask themselves: Do I want to bet my career on a company that might shut down my studio at any moment simply because of Wall Street's preferences?

The answer is increasingly "No." And where do these people go? Some go to indie development. Some go to AI. Some leave the industry altogether.

What they take with them—their understanding of hardware limits, their intuition for real-time rendering, their obsession that anything below sixty frames per second is unacceptable—happens to be the starting point of the invisible supply chain described in Chapters 7 and 8.

No one cares. Because the bill won't arrive for another ten years.

This is the final chain of causality in this book. And the only one still unfolding.

Microsoft spent $69 billion to buy Activision Blizzard, then sent its games to its competitor's console. Sony spent over $200 million making a game that lived for fourteen days. Both companies, in different ways, did the exact same thing: treating gaming as a means rather than an end, and treating players as bargaining chips rather than customers.

This sentence was written at the end of Chapter 3. Back then, it was a preview. Now, it is a settlement.

And on the settlement bill, the line with the largest amount is not the $69 billion, not the $200 million, not the $100 billion AI capital expenditure.

The line with the largest amount is a number no one can yet calculate: When the world's two largest gaming platform holders simultaneously decide "gaming is not our core business," how big of a hole will the stress test arenas, R&D funding pools, and long-term chip orders they simultaneously tear down leave in the semiconductor supply chains and AI infrastructure of the next decade?

No one is asking this question.

But TSMC's engineers in Hsinchu might already be feeling it.

That is the story of the finale.